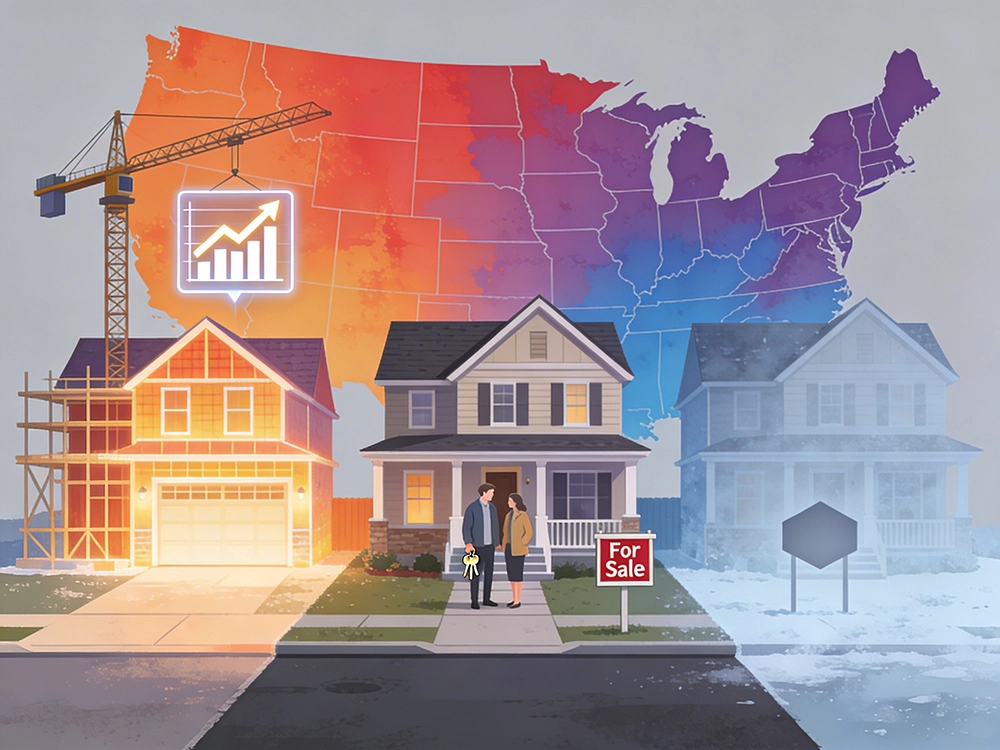

In early 2026, the American housing market defies simple labels. It is not a clear bubble, nor a clean crash. Prices sit near or above pandemic-era peaks, yet transaction volumes remain far below historical norms. Mortgage rates have come off their highs, but millions of owners cling to loans below three percent and simply refuse to move.

To make sense of this tangle, think of U.S. housing as a set of interlocking constraints: interest rates, existing homeowner behavior, construction capacity, zoning, investor activity, and demographics.

The rate shock: After a decade of ultralow borrowing, mortgage rates jumped in 2022–2023. For owners who refinanced aggressively, the gap between their current mortgage and any new loan is enormous. Selling and buying laterally can mean adding hundreds of dollars monthly for no improvement. That is the "lock‑in effect."

Lock‑in suppresses inventory, gums up labor mobility, shifts supply burden onto new construction, and creates hidden inequality between those who captured the low‑rate window and those who missed it.

Demand has not vanished: household formation continues, remote work alters where people can live. The combination of locked‑in owners and new demand pressures the thin slice of stock that comes to market.

Builders: higher interest rates make land, construction, and incentives more expensive. Zoning and permitting remain slow. New supply often clusters in suburban greenfields, priced above what median-income households can afford. In‑core neighborhoods see little new construction.

Investors: single-family rental and short-term rental landscapes are in flux. Higher financing costs and regulatory pushback have made certain strategies less attractive.

Renters face rising rents and limited paths to ownership. Affordability is about relationships between earnings and rents, between after‑rent cashflow and the ability to save.

Demographics: baby boomers hold a large share; Gen X and older millennials occupy the middle rung; younger cohorts face entry at far less favorable cost structures.

Policy: zoning reform can unlock supply, but is politically contentious. Tax policies influence ownership incentives. First‑time buyer support helps on the margin but risks bidding up prices if supply remains constrained.

The market is segmented by geography, tenure, financing history, and regulation. The puzzle is to make housing more affordable while preserving stability for existing owners and rebuilding a pathway for those on the outside.