By 2026, talking about "the U.S. energy sector" as if it were a single, coherent thing has become misleading. What exists is a patchwork: utility-scale solar and wind, natural gas plants, resurgent nuclear, brittle transmission grids, stubborn coal, and uneven EV adoption.

One way to see the change: energy has shifted from commodity cost to strategic infrastructure. Data centers, chip fabs, and EV factories negotiate power first. States that can promise reliable, clean, reasonably priced electricity have a new bargaining chip.

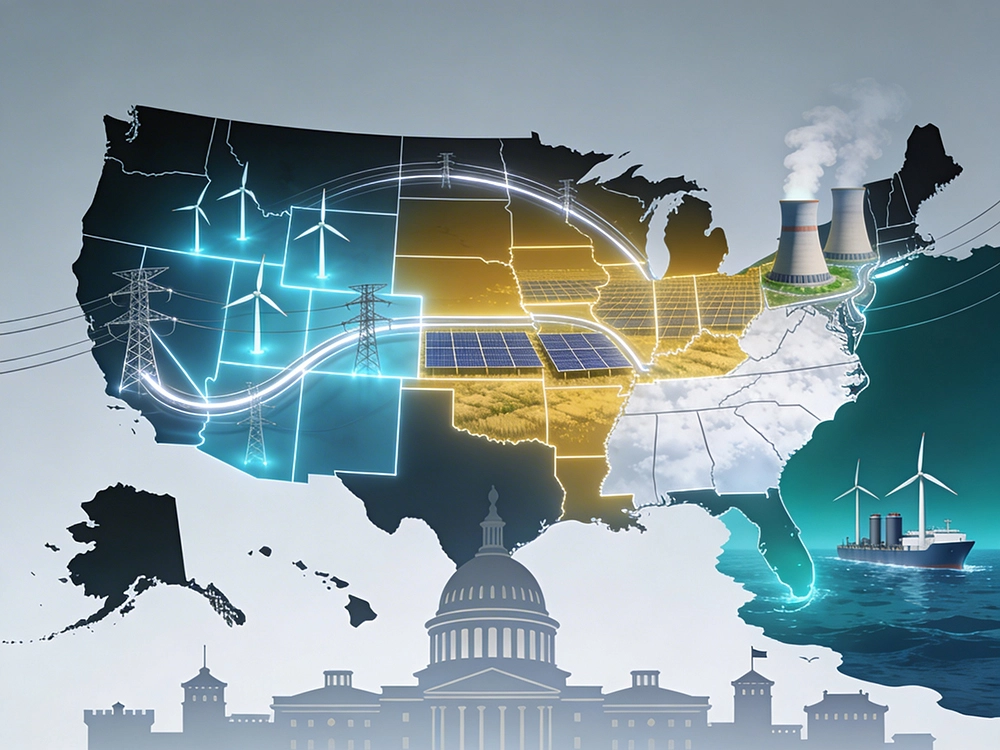

Natural gas still dominates but with a different narrative—discussed in terms of system resilience. As renewables grow and coal retires, gas plants remain the main tool for managing swings in demand or supply.

The center of gravity has shifted toward renewables and electrification. In windy and sunny regions, utility-scale wind and solar are the cheapest new bulk energy sources. The limiting factor is interconnection queues—projects wait years for studies and upgrades.

Transmission is the quiet crisis. Building new long-distance lines remains legally and politically difficult. Without stronger transmission, pockets of cheap renewable generation remain stranded.

Nuclear has reentered mainstream discussion. The old fleet still supplies meaningful electricity; small modular reactors are pitched for retiring coal sites, industrial clusters, and AI data centers.

Coal: attrition rather than revival. Most remaining plants run at lower capacity factors. Economics and public pressure lean toward retirement.

Energy storage has moved from pilot to mainstream. Lithium-ion batteries dot the grid. Longer-duration options are being tested but not deployed at scale.

Demand: EVs continue to gain share unevenly. Coastal metros see dense EV clusters; rural and lower-income areas lag. Industry is electrifying selectively.

Trade policy and industrial policy use energy as carrot and stick. Tariffs, domestic content rules, tax credits, and export policy shape the landscape.

The U.S. energy map is becoming more regionalized: Southeast (nuclear, gas, solar), Midwest (wind powerhouses), Texas (idiosyncratic grid), West (drought, wildfire, solar), Northeast (high prices, offshore wind).

Energy is no longer just a background input. It is a central variable in where companies build, where people live, and how the U.S. meets its climate commitments.